“Maduro on the Brink” was Drudge’s top headline Jan. 23, 2019. We wondered how companies operating in Venezuela account for risks.

Watchdog’s Concerns

Halliburton has been one of the largest investors in Venezuela. It took impairments of $647 million in 2017 and $265 million in 2018. What was more surprising was Halliburton had previously taken impairments of $3.4 billion in 2016 and $2.2 billion in 2015. These large impairments prompted us to ask how it was that HAL did not identify any historical errors in its prior financials or acknowledge any adverse internal controls or ineffective disclosure controls?

Given their scale and diverse nature, one would have expected some part of these impairments to have triggered restatements for prior periods.

HAL announced these impairments in the opening of their 2017 10-K along with a 33% decline in revenue and a whopping $6.5 billion loss in 2016, with this “big bath” impairment disclosure:

Our results reflected the negative impact of global activity and pricing reductions, combined with $3.4 billion and $2.2 billion of impairments and other charges recorded in 2016 and 2015, respectively.

All told, from 2015 to 1q 2018 Halliburton wrote down $6.5 billion in assets. Here’s the thing: Halliburton failed to even remotely signal ANY weaknesses in its internal controls even as they were taking these massive impairments. In fact, they gave themselves an “effective controls” score:

Under the supervision and with the participation of our management, including our chief executive officer and chief financial officer, …we believe that, as of December 31, 2017, our internal control over financial reporting is effective.

How is it that HAL can write-off $6.5 billion in assets over three years and also declares their controls to be effective? It is hard to reasonably reconcile these two opposing views. There are very few companies in the S&P 500 who have done zero restatements or who have not acknowledged some weaknesses in their internal controls for 14 years.

We wondered how a CFO would have given themselves a clean assessment given the magnitude of these issues. Turns out Halliburton had 5 CFOs in 3.5 years (see table next page). Such turnover signals trouble. Did the CFOs leave because they were overwhelmed and burned out from managing HAL’s complex reporting and business environment? Or did conflict arise over some areas of financial reporting?

This table tracks the CFO changes at Halliburton. There have been five different CFOs at Halliburton since June 30, 2016.

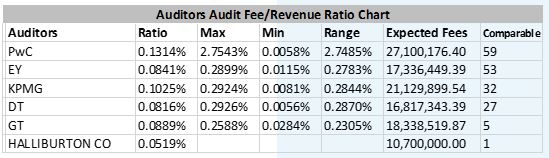

One way to off-set risks from high CFO turnover is through an increased auditor presence. Unexpectedly, HAL’s audit spending fell into the low-end of expectations. According to our peer analysis (see table on the next page), we expected HAL’s audit fees to be twice what they are now.

This table compares the audit fees paid by Halliburton to its auditor KPMG (last line) to benchmark audit fees paid to auditors by related peers of Haliburton. We benchmarked fees against revenue and calculate the normal/expected fees Halliburton would pay against each benchmark (Expected Fees column). Net/net: Halliburton’s $10.7 million in audit fees is significantly below the norms. Fees this far below the norms suggest that Halliburton’s auditor does not have the resources one would expect for this business size.

Our readers should start to recognize a pattern when they see red or yellow flags on our Watchdog Reports. First, check for stability in the CFO’s office, then assess the resources deployed for auditing and audit committee members. Then look to the SEC’s oversight. This gives insights into the overall assessment of the quality of the company’s financial reporting. In HAL’s case, we found industry and tax talent on their audit committee, but not extensive accounting and auditing talent.

What about the SEC? We were pleased to see extensive comment letters from the SEC covering 2015, 2016, and 2017. That shows the SEC was on the case. The SEC asked about many variables in their many letters (see SEC letter section in the attached HAL Watchdog Report). Lastly, in 2017 we found the SEC forced HAL to pay a $29.2 million fine to settle a Foreign Corrupt Practices Act for illegal activity in Angola.

Summing it up: HAL seems to be in an elite category of companies who have not had to correct any financial historical errors or who have not disclosed any adverse internal controls or ineffective disclosure controls for at least 10 years. Yet, HAL operates in a complex business which drives a difficult financial reporting environment. It has extensive CFO churn, billions in diverse impairments, a history of SEC questions about disclosures, an auditor paid materially less than what one would expect, and a history of fines for illegal corruption activity. It seems these two realities cannot co-exist which should lead any interested party to be wary of the quality of financial reporting at Halliburton.