The US-based PG&E is teaching the world that utilities are not boring. In the midst of the upheaval at PG&E, we noticed a change in CEO at ELP and decided to take a closer look. The results were unfortunately predictable from a BRIC country. Insider trading appears rampant and ELP is under pressure from government, judicial and legislatures. How did we come to that conclusion?

Companhia Paranaense de Energia - COPEL or the Energy Co. of Parana, is an electric utility company in the state of Parana, Brazil. It uses hydro-electric dams and transmission lines to deliver electricity to its customers. Pretty straightforward, right?

Watchdog’s Concerns

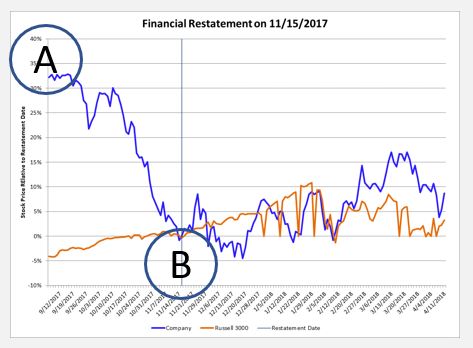

Announcing a fourth CEO in two years always raises concerns, particularly when governing authorities are involved in the selection process. We tried to figure out whether there were any precipitating events for the ouster. ELP’s price/reporting event timeline chart from ELP’s Corporate Watchdog Report shows a 32% decline in share price occurred roughly from September 12, 2017 to November 15, 2017. On November 15, 2017 (B) the company filed a 6-K form with the SEC. 6-Ks are filed as a “catch-all” notification to the SEC for out of period material disclosures. In this case, the disclosure was an expected delay of ELP’s quarterly filings.

Here are the details from the company’s 6-K filing:

The Board of Directors, after analyzing the draft of the Financial Statements for the third quarter of 2017 (ITR 3Q17) and, based on issues related to the financial statements of UEG Araucária Ltda. - UEGA, a company controlled by one of the Company’s wholly-owned subsidiaries, complied with the recommendation of the Board of Executive Officers of Copel (Holding) and the Statutory Audit Committee not to file the Financial Statements for the third quarter of 2017 (ITR 3Q17) within the period established in CVM Instruction 480/09. The Board of Directors has requested that the Board of Executive Directors expedite the completion of the work in order to inform the market promptly.

Hmm. But what happened BEFORE the board’s incomprehensible disclosure? Note the chart below details ELP’s stock price relative to the Russel 3000. Given the seemingly steep decline, one would have to ask whether there was any leakage of negative information between Sept 12, 2017 through November 15, 2017?

Later in mid-April, 2018 the company provided more information about the disclosures provided on November 15th 2017:

…requires additional time to complete the disclosure in the 2017 Annual Report related to the investigations into an investment made by its indirect subsidiary UEG Araucária Ltda. in violation of the Company’s investment policies and the recognition of a provision for the impairment of such investment in the Company’s financial statements, which were disclosed in notices furnished to the Commission on Form 6-K on November 14, 2017, November 24, 2017 and April 12, 2018.

Now this restatement disclosure was much more informative than the earlier one. The first disclosure was hard to understand. This one was clear. In particular it raised the specter that somehow senior management was involved in irregular acts-hence resignations at the top.

One month later, May 15, 2018 (C), the company released its 20-F (Foreign Filer Annual Report). The annual report threw two flags on the Watchdog Report for inappropriate disclosure controls and internal controls. Our analysts detailed the disclosure and internal controls failures as:

-

Material weakness

-

Recent or pending restatement

-

PPE , intangible or fixed asset valuation

-

Liabilities, payables, reserves and accruals

-

Foreign, related party, affiliated or subsidiary

-

Debt, quasi-debt, warrants & equity issues

-

IT, software, security & access issues

This is a healthy list of failures but seemingly these internal control failures pale next to the liability and reserve disclosures in ELP.s commitment and contingencies sections. The Company has provisioned $407 million for probable legal remedies. This on a market cap of $2.25 billion (18%). They suggest there may be another roughly $1 billion in liabilities lurking out there tied to legal issues as well. These other liabilities are likely real but unestimable–a requirement for disclosure.

Fortunately for investors, because ELP trades on the NYSE, the SEC seemed to be paying attention to the gyrations of the company and they sent the company a letter requesting additional information on August 16, 2018 (D). Our Watchdog Analysts noted the following issues requested for clarification by the SEC:

-

Revenue recognition issues

-

Commitments, contingencies, and related disclosure issues

-

Questions about fair value measurement and estimates

-

Reportable operating segments disclosure and reconciliation issues

-

Liabilities, payables, and accrual estimate issues

The company was quick to respond and the SEC finalized their analysis of the identified issues about a month later on 9/21/2018. The last SEC letter to the company seemed to indicate the SEC was not planning on taking any actions against the company. For better or worse, since that time the SEC letter seems to have lulled the market into a period of slowly increasing stock price for ELP. We also noted that the auditors seem to be doing more work, as auditor fees rose 18% from 2016 to 2017, with an additional increase expected by us for 2018.

In summary, we understand why ELP wants to trade on the NYSE and other international exchanges. As a Brazilian utility they can access financial capital markets. But there is a quid-pro-quo that comes with being traded on the NYSE. The company has to properly manage disclosures and treat all investors fairly. It is axiomatic that countries that are challenged to view investors and companies as anything other than deep pockets or sources of funds to accomplish whatever their agendas are going to continue to flounder both nationally and internationally. ELP should have a much higher share price and standing in the the market place.