Marcum BP is a joint venture between Marcum LLP and Bernstein & Pinchuk LLP specializing mostly in Chinese clients. Their practice of “city-swapping” raises some interesting questions.

UPDATE: Marcum BP was unable to make any official comment on this story. However, we did learn a great deal more about Marcum BP after publishing our article and we would like to provide that context here. As well as point out a few corrections or clarifications in the body of the article itself.

Our research is data driven and atypical results and outliers generally raise red flags. This sort of data-based analysis can tell you that you are looking at something different or unique, but it does not provide an explanation for outlying results.

When we wrote this article there was an assumption that comparing Marcum BP to other auditors would provide an apples-to-apples comparison, but the truth is far more complex. In short, it is possible that Marcum BP’s results are unique because the firm is unique.

Marcum BP is a U.S. firm that audits Chinese companies. That means Marcum BP stands behind their audits and are ultimately accountable for them. In contrast, the Big 4 have fenced off their Chinese affiliates. Our research indicates a U.S. branch of the Big 4 has not offered an audit opinion of a Chinese company since 2015, instead their Chinese affiliates handle their Chinese clients, and—unlike Marcum BP—these Chinese affiliates of the Big 4 are not subject to inspection by the PCAOB.

Other small U.S. auditing firms that provide audit services for Chinese companies often have a Chinese audit firm participate in the audit opinion to some extent. These Chinese audit firms are not subject to inspection by the PCAOB either. In contrast, Marcum BP does not partner up with Chinese audit firms to do their work in China, they do it themselves. This makes Marcum BP stand out amongst their peers.

Two final points of context. Firstly, by law Marcum BP is subject to inspection by the PCAOB at least every three years, however, the PCAOB can impose additional inspections at any time. There is no evidence that Marcum BP is attempting to avoid inspections. Marcum BP’s concentration of reports out of its New York office in 2018 may not relate to the PCAOB 2018 inspection. If it did, it would probably indicate that Marcum BP was trying to make itself more available to the PCAOB, not less.

Finally, the U.S. and China impose contradictory demands on audit firms. The Big 4 handle this problem by keeping their U.S. and Chinese operations separate, where as Marcum BP and some other small firms attempt to navigate between Scylla and Charybdis at their own peril.

Multiple solutions have been offered to this problem. The Senate unanimously passed the Holding Foreign Companies Accountable Act (yet to be voted on in the House) which would delist Chinese companies that were not inspected by the PCAOB within three years.

Carson Block argued that the Big 4 audit firms should be liable for the actions of their global affiliates because of their use of the brand. A recent report issued at the direction of the White House has recommended co-audits, which would also make the Big 4 potentially liable.

Of course, there are many who benefit from the status quo, so it is possible the Senate bill will be quietly scuttled, and the proposed reforms will be given nothing more than lip-service.

Our research team has always taken a keen interest in China, and our interest surged again with the news of Luckin Coffee’s collapse. There are several reasons why investing in Chinese companies has always been risky, but one of the most significant and ongoing reasons for being wary of Chinese companies is that Chinese auditors are supposed to be subject to inspection by the Public Company Accounting Oversight Board, or PCAOB, but the Chinese Communist Party (CCP) refuses to allow inspectors to do that job. This is because the CCP considers the work papers produced by these auditors for their China clients, often state-owned companies, “state secrets.”

Marcum BP “City-Swapping”

We wanted to know if any China-based companies listed in the U.S. had changed their auditors from U.S. member firms to Chinese member firms, perhaps to avoid auditor inspection by the PCAOB. We found a handful of companies whose audits had moved to China, but strangely enough they had not switched audit firms; instead their auditor, Marcum BP, appeared to switch office locations where the reports were issued between China and the U.S.

Every firm registered with the PCAOB must complete Form AP when issuing an audit report. The firm must include the location of the office that performed the work and issued the report by providing the city where the office is located. Marcum BP appears to have three main offices—one in New York, and two in China. (Correction: The PCAOB inspection report for 2018 indicates there are 7 offices, however New York, Beijing, and Guangzhou are named most often in the Form AP Data). We were surprised to see that some of Marcum BP’s clients “city-swapping” their opinions, alternating between New York and Beijing in successive years.

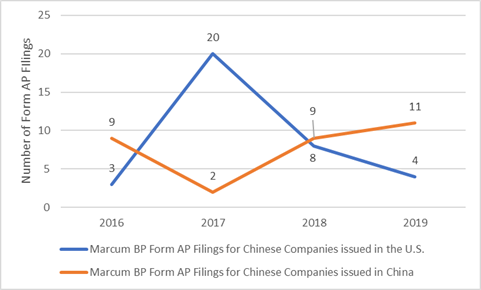

We dug more deeply into the numbers and found that since 2017 Marcum BP has signed audit reports for 37 individual companies, of whom 27 are Chinese clients. Of those clients, twelve of them had a year where the location of the office issuing the audit report for the company appeared to change countries.

This graph shows Marcum BP audit reports issued from China and the US from 2017 to 2020 year-to-date for their Chinese clients. The data indicates that Marcum BP generally issues more audit reports from its China office locations than it does in New York, except for 2018 when almost all their reports were issued out of New York. This data was derived from AP Form Data made available by the PCAOB.

We did not see any other auditors where audit opinions would switch back and forth from China (including Hong Kong) to the U.S. from 2010 to the present. Ernst and Young had one client switch from Hong Kong to Seoul in 2016, and PWC had on client, Nord Anglia Education, Inc. move from China to the UK. In short, we believe this “city-swapping” phenomenon between the U.S. and China is unique to Marcum BP.

Does a 2018 PCAOB Inspection Explain Marcum BP’s City-Swapping?

Clarification: It is possible that Marcum BP has been inspected by the PCAOB since 2018, and that the PCAOB has not issued an inspection report yet. If that is the case, then it would belie any idea that inspections and “city-swapping” were related.

Marcum BP is a small boutique firm that has never issued more than 25 reports in a given year. One advantage to being a smaller firm is that you are not subject to annual inspections by the PCAOB. Instead firms with less than 100 opinions for public companies each year are subject to inspection every third year. The PCAOB conducted an inspection of Marcum BP in 2018 and partially released the results of that inspection in January 2020.

It is well-established that the CCP has forbidden auditors operating in China to share their work papers with the SEC or PCAOB. That has created some friction between the PCAOB and the Big 4 audit firms. The Chinese member firms of the Big 4 — Deloitte, PwC, Ernst & Young, and KPMG, as well as the former BDO affiliate even faced potential sanctions by the SEC for refusing to cooperate with PCAOB inspections and SEC investigations.

In 2015, the SEC censured the firms, which eventually began providing some documents related to specific cases. Under the settlement, the firms each agreed to pay $500,000 and admit that they did not produce documents before the proceedings were instituted against them in 2012. However, they have never allowed the PCAOB to come to China and inspect the firms or perform joint inspections with Chinese authorities. In early 2020, the PCAOB removed a Memorandum Of Understanding (MOU) with China regarding how these inspections might begin to take place from its website, saying that the MOU had been ineffective.

The Big 4 firms get around the problem of uninspectable China member firms by assigning the opinion for almost all China-based company audits to Chinese member firms. What happens in China stays in China…

Marcum BP faces a different dilemma. If workpapers for client work done by its Chinese locations are not provided to the PCAOB, then the firm risks deregistration by the PCAOB, a lethal blow for a smaller firm. However, if their Chinese locations share their Chinese client’s information with the PCAOB, then the firm may invite trouble with the CCP for sharing “state secrets.”

Additionally, having the Marcum BP LLP lead engagement partner for the China-based audits work out of New York when the company’s operations and field auditors are in China is a recipe for poor audit quality.

The “city-swapping” may be a workaround to handle the firm’s dilemma.

During 2018, Marcum BP appears to have brought most of their work from China back to New York so they could issue their reports out of that office, subject to inspection by the PCAOB. In other years, most of their reports came out of their office in Beijing.

Marcum BP’s next inspection is due in 2021, and it will be interesting to see if the number of reports coming out the New York office shoots up or continues its current trend.

Power Concentration in Beijing

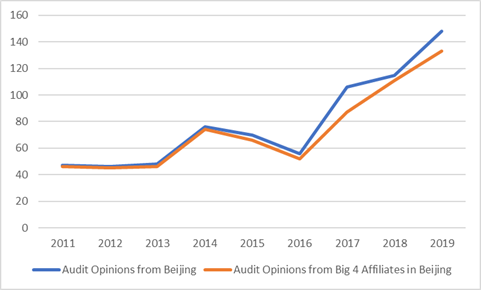

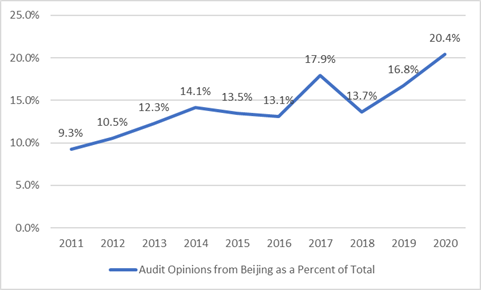

Marcum BP’s trend towards having more opinions issued out of Beijing is consistent with industry wide trends in the past few years. When we look at the city locations of the audits performed by the Chinese affiliates of the Big 4, as well as all audits performed in China, we can see a dramatic turn towards Beijing.

In absolute numbers, the number of audit opinions coming out of Beijing has risen dramatically in the last four years.

Not only are more audit opinions being issued from Beijing, but Beijing’s share of all audit opinions being issued in China has risen as well.

(These graphs were created by our data scientist Joseph Burke PhD using the audit opinions data from Audit Analytics.)

Part of what is driving this trend is that audits that were traditionally done someplace else, like in Hong Kong, are now being performed in Beijing. This concentration of power in the accounting profession mirrors the political developments in Hong Kong.

Another part of what is driving this trend is that newly listed companies are increasingly based out of Beijing. This could indicate that one of the prerequisites for a Chinese company to be successful in accessing the U.S. market is the patronage or blessing of Beijing.

The concentration of power in Beijing does not bode well. Auditors in Beijing are potentially under significantly more political pressure from the Party than those in Hong Kong. Additionally, the partners located in Beijing are also more likely to be active Party members, creating a potential conflict of loyalty when they are auditing a Party-owned enterprise.

Audit Quality Suffering

Marcum BP was subject to inspection in 2015 and the PCAOB did not appear to find any issues that made it into the publicly disclosed report. In short, they got a clean bill of health. Their 2018 inspection report, however, had very different results. The PCAOB found serious problems with Marcum BP’s audit of one issuer (likely a Chinese-based issuer).

In that report the PCAOB identified seven different areas where the issuer was significantly deficient. The lack of sufficient testing to establish effective internal controls over financial reporting (ICFR) featured prominently in the report. According to the PCAOB, “[I]n this audit, the auditor issued an opinion without satisfying its fundamental obligation to obtain reasonable assurance about whether the financial statements were free of material misstatement and the issuer maintained effective IFCR.”

That was not the only bad news that Marcum BP received from the PCAOB. In September 2019, the PCAOB fined the firm $50,000 to the firm for practices in 2013 and 2014 that had undermined auditor independence. Marcum BP had participated in conferences where they had promoted seven of their audit clients to potential investors, creating conflicts concerning their auditor independence.

Marcum BP was not alone; Marcum LLP also was assessed a $450,000 fine relating to the same conferences. The PCAOB singled out Marcum BP and Marcum LLP for this auditor independence issue, even though Francine Mckenna of The Dig has pointed out that audit firms have held similar conferences in the past that included audit clients.

Conclusion

There may be some other explanation for the apparent “city-swapping” that has nothing to do with the PCAOB inspections. The firm may simply be filling out their forms incorrectly. The have yet to respond to our inquiries.

The PCAOB and the CCP’s directives are directly contradictory, which is why our reports assign every Chinese company a red flag. It should not be surprising that auditors are contorting themselves into pretzels to stay in the good graces of the PCAOB and the CCP.

We also are not surprised that Marcum BP inspection report showed a myriad of problems with one of their clients (likely a Chinese company); the obstacles to having an adequate audit of a Chinese company are significant. We would point out that it is possible that the Chinese affiliates of the Big 4 have the same significant defects in their audits as Marcum BP, but we will never know because they are not subject to inspection by the PCAOB.

Contact us:

Retail Investors get free access to our Watchdog Reports. Institutional Investors and those interested in our Gray Swan Event Factor can subscribe, or call our subscription manager, at 239-240-9284.

If you have questions about this blog send John Cheffers, our Director of Research, an email at jcheffers@watchdogresearch.com. For press inquiries or general questions about Watchdog Research, Inc., please contact our President, Brian Lawe at blawe@watchdogresearch.com.